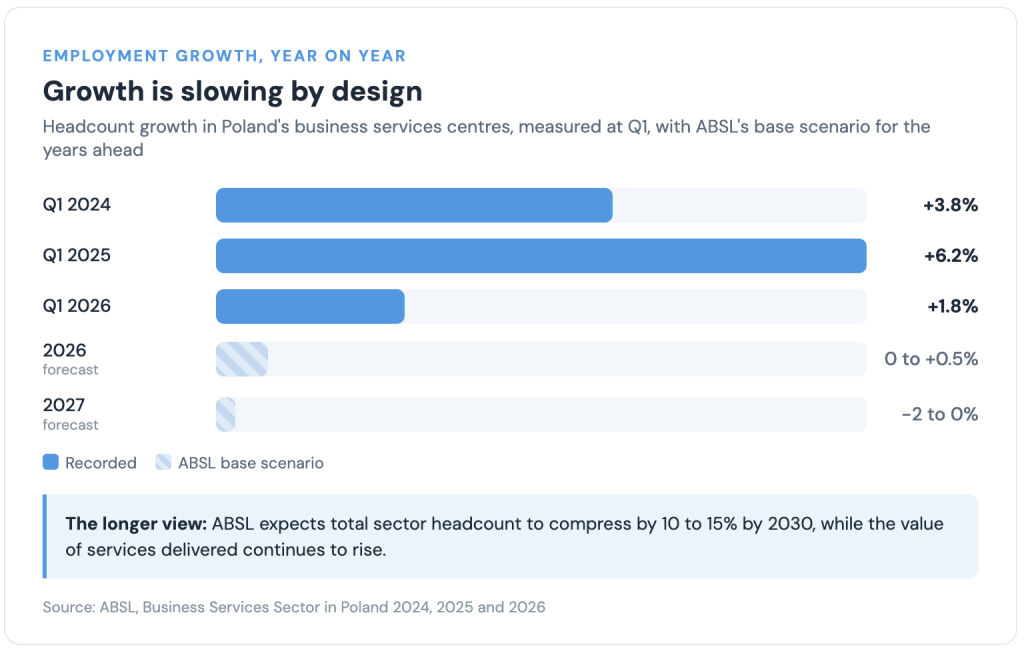

Poland’s business services sector has crossed the half-million mark. At the end of Q1 2026, 500,500 people worked across 2,179 service centres belonging to 1,303 companies, according to the Business Services Sector in Poland 2026 report from ABSL, prepared with Colliers, Mercer, Randstad and Randstad Enterprise. Employment grew 1.8% year on year, or 8,860 jobs. That is a fraction of the 6.2% ABSL recorded a year earlier, though it came against an enterprise sector where overall employment fell 0.8% over the same period.

The sector is still outgrowing the economy around it. What has changed is how it grows: less by adding people, more by getting more from the people it has.

Growth Has Slowed, and That Is the Point

Of the 8,860 new jobs, only 3,240 came from new centres: 46 opened in 2025 and four in the first quarter of 2026, the slowest pace of new openings in a decade. ABSL is explicit that the peak of greenfield investment has passed.

Growth today is organic, driven by reinvestment and by existing centres taking on more complex work.

Hiring intentions confirm the shift. Fewer than one in five employers, 18.6%, plan to increase headcount by more than 10% by Q1 2027, and analysis from The Hackett Group cited in the report forecasts workloads growing 15% this year against staffing growth of just 10%. That five-point productivity gap has to be closed with technology and better-deployed people, not recruitment volume.

The business results explain why nobody in the sector is alarmed. Exports reached a record $48.4 billion in 2025, equal to 36.9% of Poland’s commercial services exports, and exports per worker climbed to $96,700. Gross value added per worker stands at $65,200, 27.9% above the Polish economy’s average.

The sector now generates 6.1% of GDP and 7.8% of enterprise employment. Looking ahead, ABSL’s base scenario assumes employment growth of 0 to 0.5% this year and between minus 2% and zero in 2027, with total headcount expected to compress by 10 to 15% by 2030 even as the value of services delivered keeps rising.

From Talent Shortage to Skills Mismatch

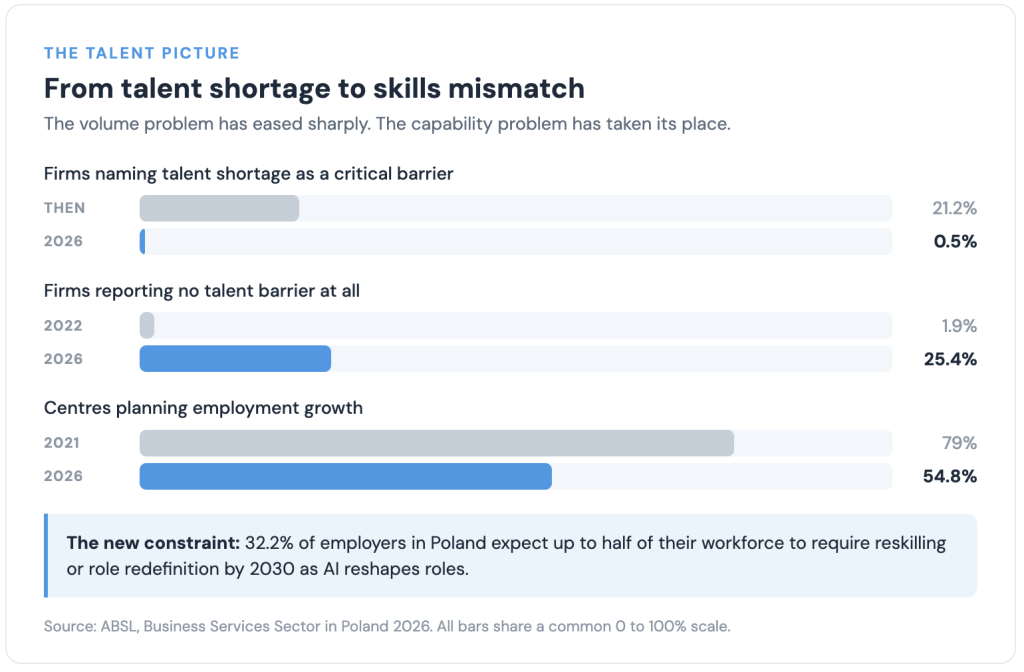

The report uses this exact phrase as a heading, and the data behind it is striking.

The share of firms naming talent shortage as a critical barrier has collapsed to 0.5%, from 21.2%, while 25.4% now report no talent barrier at all, up from 1.9% in 2022.

ABSL attributes the easing to greater organisational maturity, better retention, stabilised labour market conditions, and inflows of workers, notably from Ukraine. Hiring intent has cooled in step: 54.8% of centres still expect employment growth, down from over 79% in 2021, while 28.9% now anticipate stable headcount.

The constraint has changed shape rather than disappeared.

The work itself is moving up the value chain: mid-office functions now represent 63.4% of operations, knowledge-intensive services account for 58.2% of the workload, and back-office participation has declined to 33.3%. The workforce is maturing with it, with employees aged 35 and over now making up 51.3% of the total. And nearly a third of employers, 32.2%, expect up to half of their workforce to require reskilling or role redefinition by 2030 as AI reshapes what the jobs involve.

The challenge, in ABSL’s words, has shifted from entry-level labour availability to securing specialised, high-skill talent for knowledge-intensive operations.

What the Business Services Sector in Poland Shift Means for Employers

One more figure from the report deserves attention. Some 80% of employers in Poland have increased investment in automation or digital tools, yet 57% report no significant workforce impact.

Capability is not something a company buys with software licences. It is built through the people who integrate the technology into how work actually gets done, which is why the premium on experienced specialists keeps rising even as overall hiring cools.

For HR and talent leaders, the volume playbook is losing relevance. Scaling a Polish operation in 2026 looks less like opening a recruitment pipeline and more like assembling a capability: a precise brief, a longer search, and a hiring plan that pairs targeted external recruitment with internal mobility and reskilling.

Poland’s fundamentals remain strong, and the labour market has tilted back toward employers for the first time in years. But competition has concentrated at the experienced end of the market, and employers who still measure progress in headcount risk paying a premium for the wrong profile.

Verita HR is seeing the same shift in the mandates it receives. Briefs to fill seats at volume are giving way to requests for experienced specialists and for help building long-term capability, which is exactly the pattern the ABSL 2026 data describes across the market.

Poland remains one of the core business services hubs in Europe. What has changed is the measure of success. Employers planning their next phase of growth in the business services sector in Poland can contact Verita HR to talk through what a capability-first hiring plan looks like in practice.

Grace Sharp

See Also:

Why French Speakers Are in High Demand Across Poland’s Business Services Sector

Why Dutch Speakers Are in High Demand Across Poland’s Business Services Sector