The Czech Republic’s fintech revolution is growing. Once peripheral in Europe’s financial technology map, the country now hosts over 200 fintech companies, double the number from five years ago, spanning payments, lending, regtech, and blockchain. It’s not a hype story; it’s a story of steady evolution backed by digital-savvy consumers and cautious but real engagement from regulators and banks.

Yet, 2025 marks pivotal shifts: the launch of a national regulatory sandbox, the Czech National Bank’s (CNB) experimental Bitcoin holdings, and the full enforcement of EU-wide rules like DORA (Digital Operational Resilience Act) and MiCA (Markets in Crypto-Assets). These developments signal a maturing environment, where innovation meets compliance, potentially accelerating adoption while addressing scalability hurdles for small firms.

From Everyday Tools to Embedded Innovation: Consumer Adoption Soars

Beyond general digital banking, specific fintech tools have surged in popularity in the Czech Republic, reflecting local consumers’ openness to innovation. Mobile payments, for instance, have seen explosive growth: 54% of Czechs have tried them, up from just 19% five years ago, with the country ranking 7th in Europe for payments via mobile phones and wearables. Every second card transaction now occurs through a mobile or wearable device, and features like tokenization have doubled in adoption over the past two and a half years.

Tools such as payment rings, bracelets, Pay-to-Fuel (for gas station payments), and Pay-to-Park apps are increasingly common, enhancing everyday convenience. Personal finance management apps stand out for their user base and utility. For instance, a wallet by BudgetBakers connects to over 5,000 European banks, supports 40+ languages, and helps users track expenses and budgets seamlessly. Similarly, Spendee allows manual entries, bank linking, multi-currency support, and shared wallets, promoting financial literacy among a growing audience.

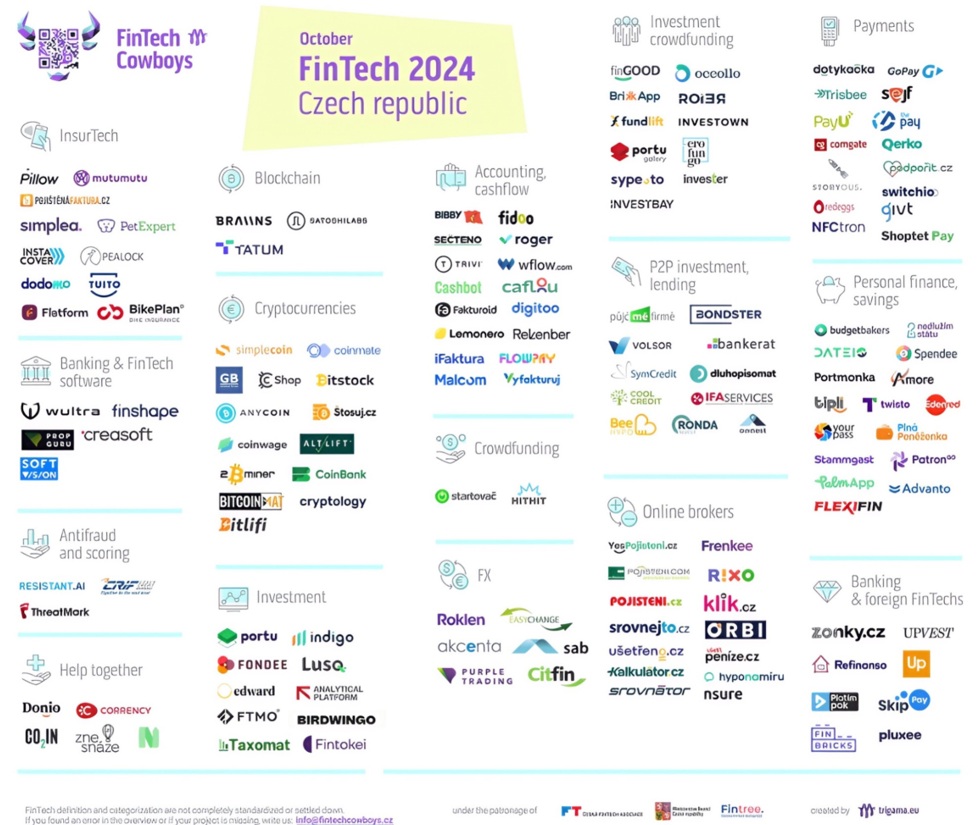

Source: Czech Trade Promotion Agency

Source: Czech Trade Promotion AgencyWealthtech platforms like Portu manage finances for over 200,000 clients, overseeing CZK 40 billion as of January 2025. Other notable tools include Banking Identity (Bank iD), used by 6.5 million customers for secure logins and verifications across banking and e-government services. The Qerko app, with 1.4 million users in the Czech Republic, Slovakia, and Hungary, enables QR-based payments, ordering, and loyalty programs in over 1,500 restaurants.

When it comes to crypto and cybersecurity, ThreatMark protects 40 million customers globally from fraud, while data enrichment tools like Tapix serve 73 million people through partnerships with 50+ banks and fintechs in 80 countries. Even cryptocurrency tools are popular, with the Czech Republic boasting the highest per capita acceptance points in Europe via gateways like Confirmo.

These tools’ popularity stems from high e-commerce penetration and consumer trust in digital solutions, with 76% of Czechs making cashless payments when cards are accepted. This consumer-driven demand complements the broader fintech ecosystem, where tools are not just adopted but integrated into daily life.

ČR: Osoby v Česku využívající finanční služby online, 2025 (zdroj: @czstatistika )

(% z celkového počtu osob v dané socio-demografické skupině, Věková skupina 16+)

Internetové bankovnictví 77,9%

Sjednání pojištění 18,2%

Nákup cenných papírů 3,7% pic.twitter.com/SsyUuRsbMO

Banks and Startups: Collaboration as the New Norm

The Czech Republic’s banking landscape is concentrated. Four major banks dominate a nation of 10.7 million. In such a small market, most fintech startups have prioritized B2B solutions rather than going head-to-head with banks. “With four big banks and a small population, B2C activities are not so common,” Ivan Dovica, co-founder and co-CEO of Tapix by Dateio, told Ergomania. “The focus is on B2B,” in the Czech Republic’s fintech scene. In practice, this means new fintech companies often develop niche solutions to sell to banks or collaborate with them, rather than trying to displace them outright.

This collaboration can be seen in examples like Twisto, a Czech buy-now-pay-later startup. Twisto began by offering consumers instant instalment payments and later evolved toward a broader digital banking app. The company has since worked with banks such as Raiffeisenbank and ING rather than positioning itself as a bank killer. That approach paid off: it drew global attention and was later acquired by Australia’s Zip for €89 million in 2021.

Tension still exists within the ecosystem. Banks once closed fintech accounts they saw as threats, prompting intervention by the local Fintech Association. Yet even those same incumbents have modernized. Today every major Czech bank offers full mobile apps and several run accelerator programs. Collaboration has replaced hostility as both sides realize they need each other: banks gain agility, fintechs gain scale. It’s a win-win.

There are some specific regulations, albeit that have helped to realize the degree of streamlined fintech operations that Czech startups enjoy today.

Regulators: From Caution to Catalyst

For years, the Czech National Bank lived by the unofficial motto “Don’t help, don’t protect.” Startups got no special treatment, no sandboxes, and no shortcuts. But since 2023, that tone has shifted.

The Ministry of Finance set up an innovation unit, the central bank appointed a fintech liaison, and Prague, working with the Organisation for Economic Co-operation and Development (OECD), is developing a regulatory sandbox for controlled fintech testing.

EU rules loom large: DORA enforces ICT resilience from January 2025, mandating audits for payment firms; MiCA shifts VASPs to authorization by year-end, gold-plating AML since 2021. Crypto leads the charge. The CNB’s November 2025 $1M Bitcoin pilot (with stablecoins and tokenized deposits) marks Europe’s first central bank crypto reserve, building on Governor Aleš Michl‘s early-2025 proposal for billions in BTC holdings. This “educational” move via CNB Lab tests blockchain for settlements, signalling readiness for digital euro pilots.

Industry leaders like Maria Staszkiewicz of the Czech Fintech Association warn that EU-level rules, especially on AI and crypto, could burden small firms with legal costs. “Startups may need lawyers before they have customers,” she noted. Still, dialogue between fintechs and regulators is improving, which is a good sign of a shift from passive tolerance to active engagement.

While the positive notch-up in fintech regulation is welcomed, an important question arises. Can Czech fintechs scale fast enough to match investor ambition?

A Balanced Path Forward: Lessons for Sustainable Growth

The Czech Republic’s fintech story is a quiet, steady one, rather than a flashy disruption. For general business observers, the main takeaway is that the country has cultivated a solid fintech foundation by leveraging its tech-savvy population and engineering talent, even while operating in the shadow of big banks and bigger countries.

For now, Czech fintechs can be viewed as a microcosm of fintech’s evolution in traditional banking markets: initial disruption meeting practical collaboration, gradual regulatory acceptance, and startups navigating how to scale beyond a comfortable niche. It may lack hype, but in many ways, that is a strength.

As Czech fintech continues its upward climb, its balanced path could offer lessons in sustainable innovation for other emerging fintech hubs. The Czech Republic might not be able to produce the next global fintech giant overnight, but it is steadily proving itself as a credible player in the financial innovation arena.

Unchain.media has taken all precautions to ensure that no persons or organizations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.